“In 42 states and DC, at least one predatory lender is using a rent-a-bank scheme to evade the law and make 100% to 225% APR loans that are illegal in those states.”

Americans for Financial Reform

When we roamed the earth as Neanderthals, our species worried about predators lurking at every turn, wanting to fatten themselves up at our expense. Today, the same dynamic exists, only now the predators are a species known as lending institutions, which have come up with a new scheme: hide behind a few unscrupulous, traditional banks to avoid state usury laws, and charge between 100%-200% + interest for items most of us need, but cannot afford to purchase outright (except puppies from pet stores—see below).

And these particular lending institutions certainly stalk their prey, by planting storefronts in the poorest neighborhoods, where they know the residents are weakened from lack of cash and desperate for credit. This is akin to the strategy of the Payday Loan lenders, which I discussed in a previous post. When have you seen loan sharks and pawn shops in a leafy suburb? Of course, the predators’ reach has grown exponentially with the proliferation of Internet banking, but the poor, working class and even middle-class borrowers in need of a loan are still targeted and pay a steep price.

Rent-A-Bank loans have been around since at least the 1990’s, and are simply a scheme to avoid the cap on interest rates that most states have enacted to protect consumers from paying insanely high rates and becoming trapped in a cycle of debt. Here is an explanation of the rent-a-bank scheme:

In the late 1990s, payday lenders started entering into “rent-a-bank” arrangements under which the payday lender marketed and took applications for loans, the bank technically approved and funded the loans, and the bank then immediately sold the loan or servicing rights back to the payday lender. The payday lender claimed that because the bank funded the loans, state interest rate limits did not apply. The National Consumer Law Center

According to a May report by “Stop the Debt Coalition” and noted in a press release by the Consumer Federation of America, national car repair shops, like Meinike, AAMCO, Jiffy Lube, Midas and local auto repair shops are advertising and even steering customers to finance through these unscrupulous lenders. If your credit cards are ready to burst and you have no spare cash, you’re forced to get financing, particularly for a necessity like car repair.

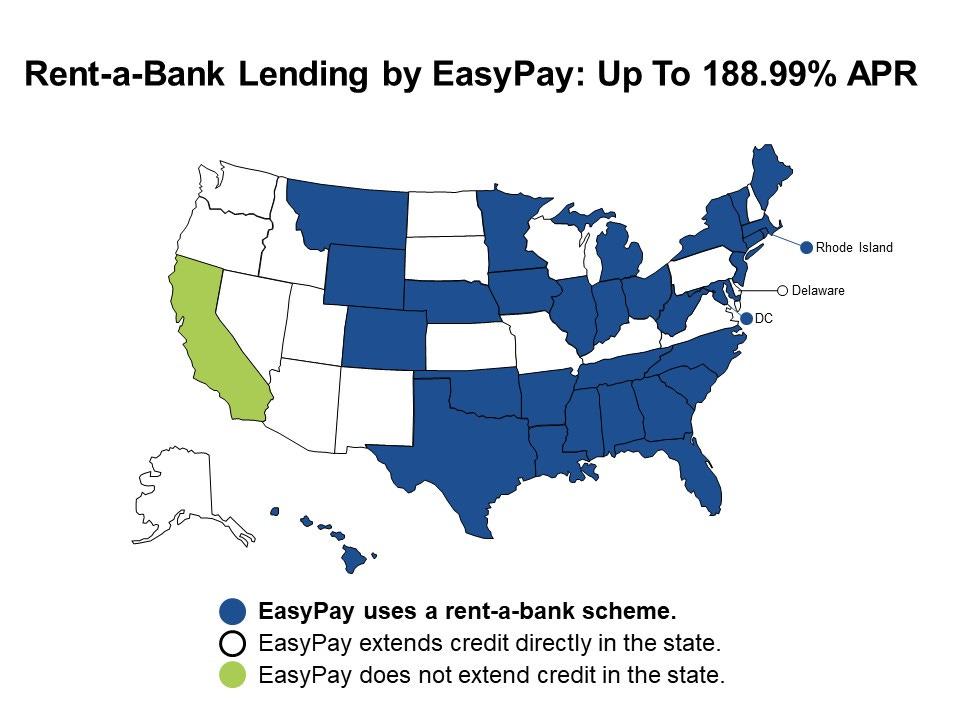

But it doesn’t stop with auto repair shops, these usury interest loans are pushed by furniture stores, other retail establishments and yes, pet stores, in nearly every state, even in those that actually enforce their usury laws. See the detailed charts in this article from the National Consumer Law Center that names some of the most prominent non-bank, predatory lenders and the FDIC regulated banks who front their scheme. The charts also show exactly in which states each unscrupulous lender does business.

Here’s a sample map for one of the biggest predatory lenders, EasyPay Finance.

The National Consumer Law Center also published a detailed piece on predatory “puppy loans”, which includes real stories of consumers who paid a small fortune for a puppy in a pet store or online, then financed that beautiful, living creature with a usury interest rate loan, ended up with a terribly sick or dead dog (because all pet store puppies are sourced from puppy mills, so of course they will be sick) and were then stalked by debt collectors wanting their 160% interest rate.

Let me digress: There is one easy way to avoid predatory puppy loans and that is to never walk into a pet store that sells live pets, unless you can be sure that each animal there is from a shelter or rescue. First, it makes me sick to realize that our society considers living creatures a product, which can be financed, no less. And I can’t believe that after decades of work by the ASPCA, The Humane Society of the United States, Best Friends Animal Society and hundreds of other animal welfare organizations and rescues, each of which have spent millions of dollars on ad campaigns, TV commercials and all sorts of outreach decrying puppy mills and their intimate connection with pet stores and online fake “breeders”, that people still pay thousands of dollars for what they think is a purebred dog in a store or online. You can get a super dog just like my crack research assistant, Bocci, at any local shelter across the country. If you must have a purebred dog or cat, please check the thousands of rescue organizations first, and then if you choose not to adopt or rescue, find a reputable breeder.

Fortunately there have been legal prosecutions of these usury rate lenders in a few states. One example is the settlement reached by the Attorney General of DC against Elevate Credit, Inc, a predatory online lender. This is a quick summary of that settlement:

Attorney General Karl A. Racine today announced that Elevate Credit, Inc. (Elevate), a predatory online lender, will pay at least $3.3 million to refund over 2,500 District consumers who were misleadingly marketed high-cost loans and lines of credit, waive over $300,000 in interest owed by those consumers, and pay $450,000 to the District. The company will also be required to stop charging rates above the District’s legal cap of 24% and to cease deceptive and misleading business practices.

Not bad, but what about the bank or banks that fronted these loans? Where is their liability? The rent-a-bank scheme circumvents the law, and in limited circumstances a few lenders have agreed to pay back monies defrauded from consumers. But I don’t believe the scheme itself is currently illegal. The underlying question, though, is why are FDIC regulated banks exempt from state usury laws that cap interest rates? There would be no scheme if all lenders were subject to state (or federal) usury laws.

I write Crime and Punishment not to tell you there are millions of people unnecessarily living below the federal poverty line in one of the richest countries on earth, that there are millions more living paycheck to paycheck and without health insurance, and that what’s left of the middle-class isn’t earning enough to buy the necessities, let alone save for retirement and send their children to college. I write this newsletter to help explain exactly why this is happening, what laws and policies need to be enacted or changed to help eliminate poverty, close the obscene economic inequality gap and foster a thriving middle class. It is our individual and collective actions that will make the difference.

I ask you to join me on our journey to understand the why behind the facts, so together we finally can find solutions to our most pressing economic issues and push to right the wrongs of our system. Each of us can thrive in this country, if we don’t allow ourselves to be beaten down by the very system we’re trying to make good in. One of the best ways to do this is to become an active member of your community and a participating citizen in our larger community.

And speaking of communities, you can also become a participating member of the Crime and Punishment community by signing up right now for a free or paid subscription.

What needs to be done to stop predatory loans with usury interest rates, and lenders who find ways to do an end around of the law? Please share your thoughts on today’s post in the Comment Section below.

And one more request: be a part of the solution by sharing this post and asking your friends to sign up for Crime and Punishment!

Thanks!

Additional Resources

A government primer on predatory lending with specific information where you can go for help if you are a victim: https://www.justice.gov/usao-edpa/divisions/civil-division/predatory-lending

Here you can look up where one of the major culprits, EasyPay Finance, does business in your area: https://findastore.easypayfinance.com/

.

Share this post